3. 経営の開放性

本項では、経営の開放性として、社外 11 への情報開示、経営課題の共有・相談の状況と効果を確認する。

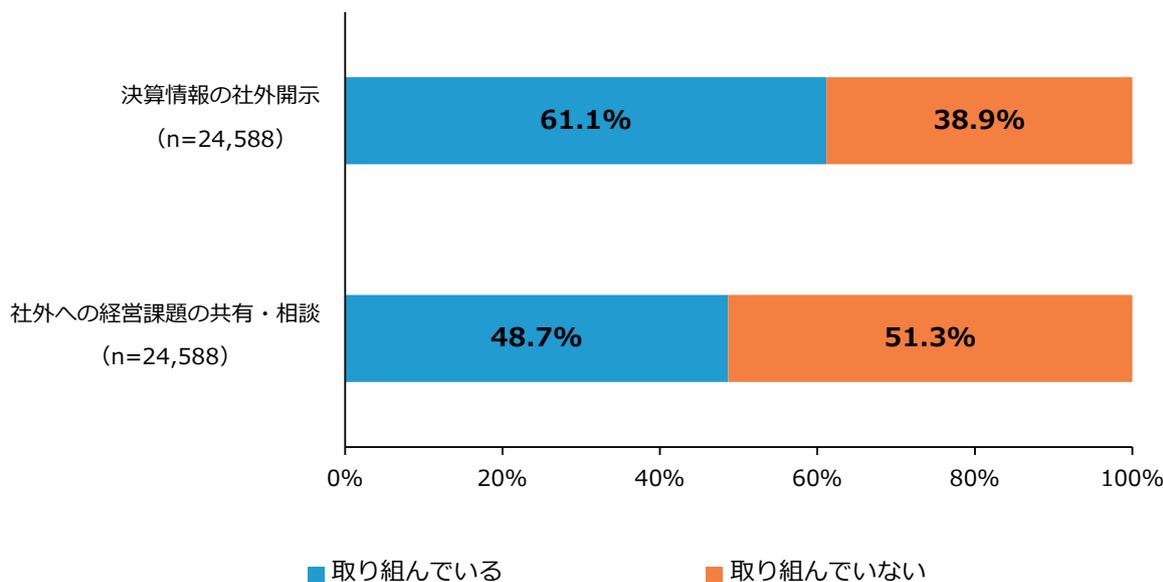

①経営の開放性への取組状況

第2-1-27図は、「決算情報の社外開示」、「社外

への経営課題の共有・相談」への取組状況を見たものである。「決算情報の社外開示」には約6割の事業者が取り組んでおり、「社外への経営課題の共有・相談」については約半数の事業者が取り組んでいることが分かる。

第2-1-27図 社外に対する経営の開放性への取組状況

| 項目 | 取り組んでいる (%) | 取り組んでいない (%) |

|---|---|---|

| 決算情報の社外開示 (n=24,588) | 61.1% | 38.9% |

| 社外への経営課題の共有・相談 (n=24,588) | 48.7% | 51.3% |

Horizontal stacked bar chart showing the percentage of businesses implementing external disclosure of financial information and sharing/consulting management issues. For financial disclosure, 61.1% are implementing and 38.9% are not. For sharing/consulting, 48.7% are implementing and 51.3% are not. Sample size n=24,588.

資料:(株)帝国データバンク「令和6年度中小企業の経営課題と事業活動に関する調査」

(注) 各取組について、「取り組んでいる」は「十分取り組んでいる」、「ある程度取り組んでいる」と回答した事業者の合計。「取り組んでいない」は、「ほとんど取り組んでいない」、「あまり取り組んでいない」と回答した事業者の合計。

11 ここでの「社外」とは、外部株主、金融機関、支援機関、有償のコンサルタント等を指す。