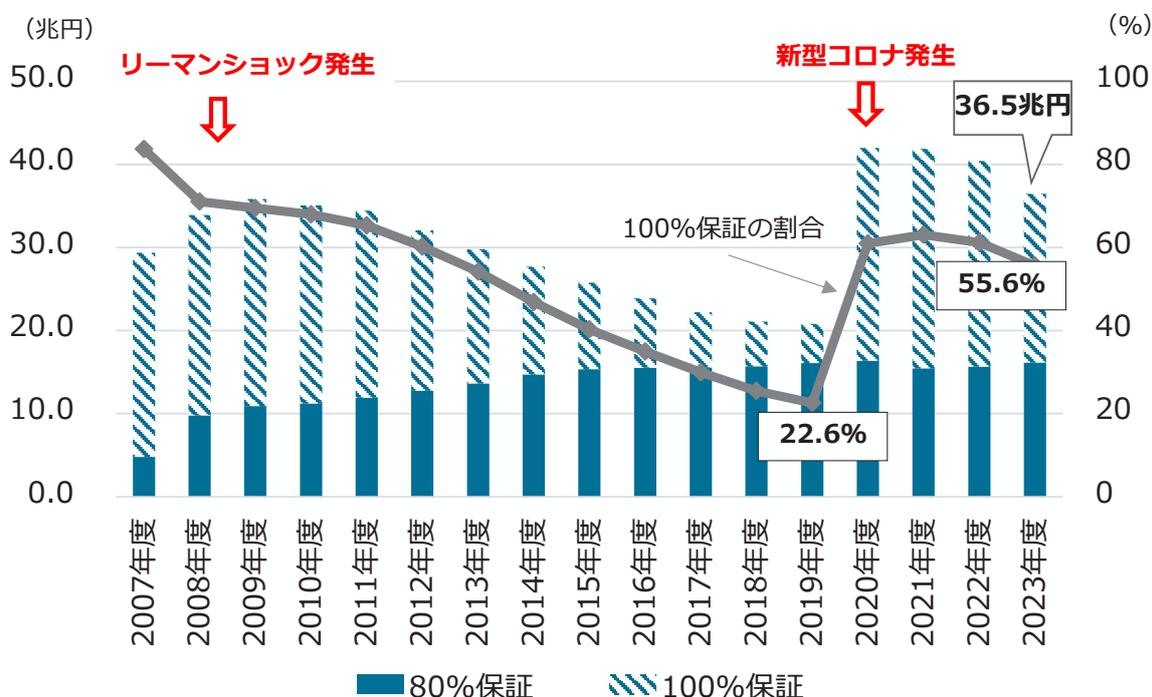

コラム 1-1-2②図 信用保証協会における保証債務残高と100%保証の割合の推移

| 年 | 80%保証 (兆円) | 100%保証 (兆円) | 100%保証の割合 (%) |

|---|---|---|---|

| 2007年 | ~4.0 | ~25.0 | ~85 |

| 2008年 | ~9.0 | ~26.0 | ~70 |

| 2009年 | ~10.0 | ~25.0 | ~68 |

| 2010年 | ~11.0 | ~24.0 | ~65 |

| 2011年 | ~12.0 | ~22.0 | ~60 |

| 2012年 | ~13.0 | ~20.0 | ~55 |

| 2013年 | ~14.0 | ~18.0 | ~50 |

| 2014年 | ~15.0 | ~16.0 | ~45 |

| 2015年 | ~16.0 | ~14.0 | ~40 |

| 2016年 | ~17.0 | ~12.0 | ~35 |

| 2017年 | ~18.0 | ~10.0 | ~30 |

| 2018年 | ~19.0 | ~8.0 | ~25 |

| 2019年 | ~20.0 | ~6.0 | 22.6 |

| 2020年 | ~16.0 | ~20.0 | 36.5 |

| 2021年 | ~15.0 | ~25.0 | ~35 |

| 2022年 | ~15.0 | ~24.0 | ~35 |

| 2023年 | ~16.0 | ~23.0 | 55.6 |

資料:(一社)全国信用保証協会連合会提供資料より中小企業庁作成

(注) 1. ここでいう「80%保証」、「100%保証」とは、信用保証協会による債務保証割合のことであり、80%保証(負担金方式の場合)では、信用保証協会は金融機関から20%の負担金支払いを受ける。

2. 「100%保証の割合」 = 「100%保証」 ÷ (「80%保証」 + 「100%保証」)。

2. モニタリングの在り方

感染症の感染拡大時に講じた民間ゼロゼロ融資は、融資先の経営状況にかかわらず緊急避難的に政府がリスクを取り、資金繰り支援を行うものであった。そうした結果、「100%保証」をはじめとする保証付融資が増加するとともに、保証申込時にプロパー融資(保証を伴わない融資)を伴う割合は減少した。望まない廃業・倒産や地域経済への悪影響を防ぎながら、経営状況の回復及び成長・持続的発展を目指す事業者を後押しするためには、適切なモニタリング体制を構築し、経営状況の変化の予兆を早期かつ即時的に捉えて、適切な事業者支援につなげていくことが重要である。

このためには、①事業者が必要なデータを生成し、そのデータを信用保証協会・地域金融機関・支援者(士業、政府系支援機関、その他専門家等)が取得する、②当該データを基に信用保証協会・地域金融機関・支援者が予兆管理を行う(予兆フラグの検知)、③関係者で連携しつつ必要な事業者支援を行う、といったモニタリングの流れの中で、事業者と関係者間の対話等も通じて、事業者が自らの経営状況を適切に把握することの重要性を認識するとともに、初期段階で経営課題に気付き、支援を受け入れて経営改善に取り組む必要性について理解(腹落ち)するなど、事業者自身の行動変容につなげていくことが重要である。